Immune-Based Gene Therapy Candidates Should Prevail In Oncology, Says GlobalData

Gene therapy combines a reduced treatment duration with a higher chance of cure unlike conventional oncology treatments such as chemotherapy. However this novel therapeutic approach requires the delivery of genetic material to the patient, an uncharted territory in oncology which will necessitate the implementation of new regulatory guidelines and the restructuring of existing treatment algorithms in various oncology indications says GlobalData, a leading data and analytics company.

The company’s latest report; ‘Gene Therapy in Oncology’ provides an overview of the current competitive landscape of gene therapies in oncology and the regulatory framework concerning their clinical development and commercialization across the 8MM*. In addition, the report covers in detail the Phase III and Phase II cancer gene therapy candidates that are expected to enter the oncology space within the next decade and provides key opinion leader insights on the impact of cancer gene therapies in various treatment paradigms in the oncology space as well as a payer perspective on the cost and reimbursement of novel cancer gene therapies.

The current clinical development of gene therapies in oncology is dominated by small size biotech and pharmaceutical companies. AstraZeneca is the only large pharmaceutical company with an in-house gene therapy in late stage clinical development. Other major players such as Johnson & Johnson, have the exclusive worldwide rights to develop and commercialize Geron’s imetelstat, while Merck & Co. and BMS are evaluating their respective checkpoint inhibitor therapies with many of the Phase III and Phase II candidates in the cancer gene therapy pipeline.

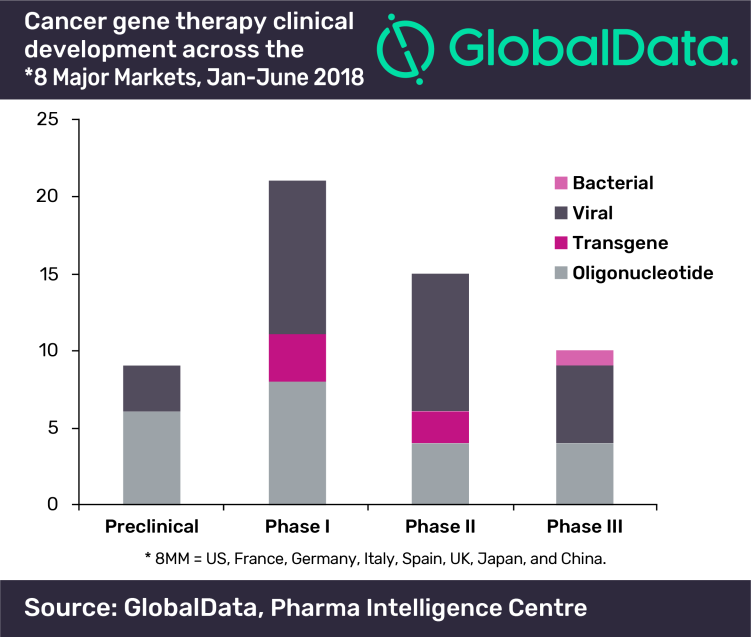

Viral gene therapies dominate the late stage pipeline. There are 25 gene therapy candidates in clinical development in a variety of oncology indications. The most commonly targeted tumor types include melanoma, which is highly responsive to immunotherapies and hard-to-treat tumors such as CRC, GBM, pancreatic, and prostate cancers.

IMAGE FOR PUBLICATION: ‘Cancer gene therapy clinical development across the *8 Major Markets, Jan – June 2018.’

Oligonucleotide and viral gene therapies dominate the Phase III pipeline while oncolytic viral gene therapies are more commonly represented in the Phase II pipeline. In contrast, there is limited clinical development of other types of gene therapies such as bacterial gene therapies and transgenes.

Volkan Gunduz, Senior Oncology and Hematology Analyst at GlobalData, commented: ’Ample opportunity remains in the oncology space for gene therapies. One of the most promising therapeutic strategies is developing combination regimens of gene therapies with immune checkpoint inhibitors. To this end significant opportunity exists as half of the Phase III pipeline is evaluated as a monotherapy and only one candidate is evaluated in combination with a checkpoint inhibitor.’

The use of novel cancer gene therapies in combination with immune checkpoint inhibitors will provide more clinical benefit to cancer patients, increasing treatment durations significantly. The high cost of novel therapies and longer treatment durations are major factors that will increase the cost of care in the oncology space.

Gunduz added, ‘‘The concept of cancer gene therapy is not well established among payers and the already significant share of oncology in healthcare spending will prompt payers to come up with innovative approaches to contain the cost of novel cancer gene therapies. Payers point to the current lack of effective tools to contain the cost of newly approved oncology treatments.’’

Information based on GlobalData’s report, ‘Gene Therapy in Oncology’

Information based on GlobalData’s Report: Hot Topic: ‘Gene Therapy in Oncology’

The report covers: an overview of the current competitive landscape of gene therapies in multiple oncology indications, the regulatory framework concerning their clinical development and commercialization in the 8MM, the late stage clinical development of cancer gene therapies in the 8MM and key opinion leader (KOL) insight on the impact of cancer gene therapies in various treatment paradigms in the oncology space as well as payer perspective on the cost and reimbursement of novel cancer gene therapies. For the purpose of this report, GlobalData defined gene therapy in oncology as therapies that consist of oligonucleotide agonists, antisense oligonucleotides, oncolytic and transgene expressing viruses, DNA and mRNA based transgenes, and bacterial therapies.

About GlobalData

4,000 of the world’s largest companies, including over 70% of FTSE 100 and 60% of Fortune 100 companies, make more timely and better business decisions thanks to GlobalData’s unique data, expert analysis and innovative solutions, all in one platform. GlobalData’s mission is to help our clients decode the future to be more successful and innovative across a range of industries, including the healthcare, consumer, retail, financial, technology and professional services sectors. PR2020

‘*’ 8MM = US, France, Germany, Italy, Spain, UK, Japan, and China.

Source: GlobalData